We use cookies to improve your experience. By using BondbloX, you agree to our use of cookies.

Bond Market News

ISM Services PMI Decelerates to 54.0

April 7, 2026

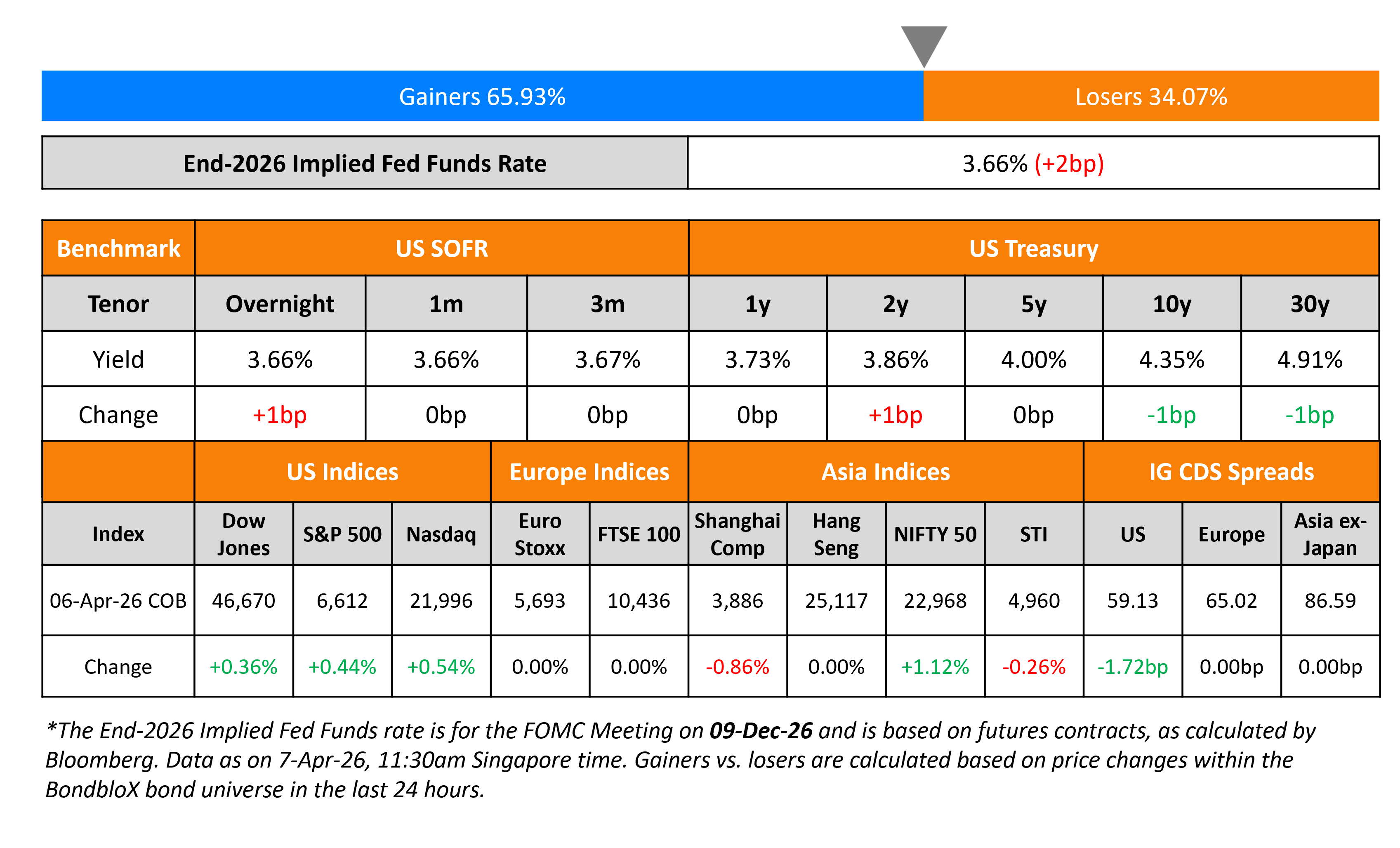

US Treasury yields held steady across the curve. The ISM Services PMI for March continued to show an expansion in the sector, albeit at a slower pace. The reading came in at 54.0, softer than expectations and the prior reading of 54.9 and 56.1 respectively. Among its sub-components, the Employment Index contracted, dragging the overall reading while the Prices Paid and New Orders components helped offset the former’s impact. Regarding inflation, Cleveland Fed President Beth Hammack and Chicago Fed’s Austan Goolsbee indicated that inflation was a bigger problem than employment and potentially flashing “orange”. On the geopolitical front, US President Donald Trump threatend to destroy Iran’s infrastructure, including bridges and power plants, if they do not agree to a deal today.

Looking at US equity markets, the S&P and Nasdaq ended higher by 0.4-0.5% on Monday. US IG CDS spreads tightened by 1.7bp while HY CDS spreads were 7.4bp tighter. European equity indices and CDS markets were closed yesterday due to Easter Monday. Asian equity markets have opened mixed this morning. Asia ex-Japan CDS spreads were flat.

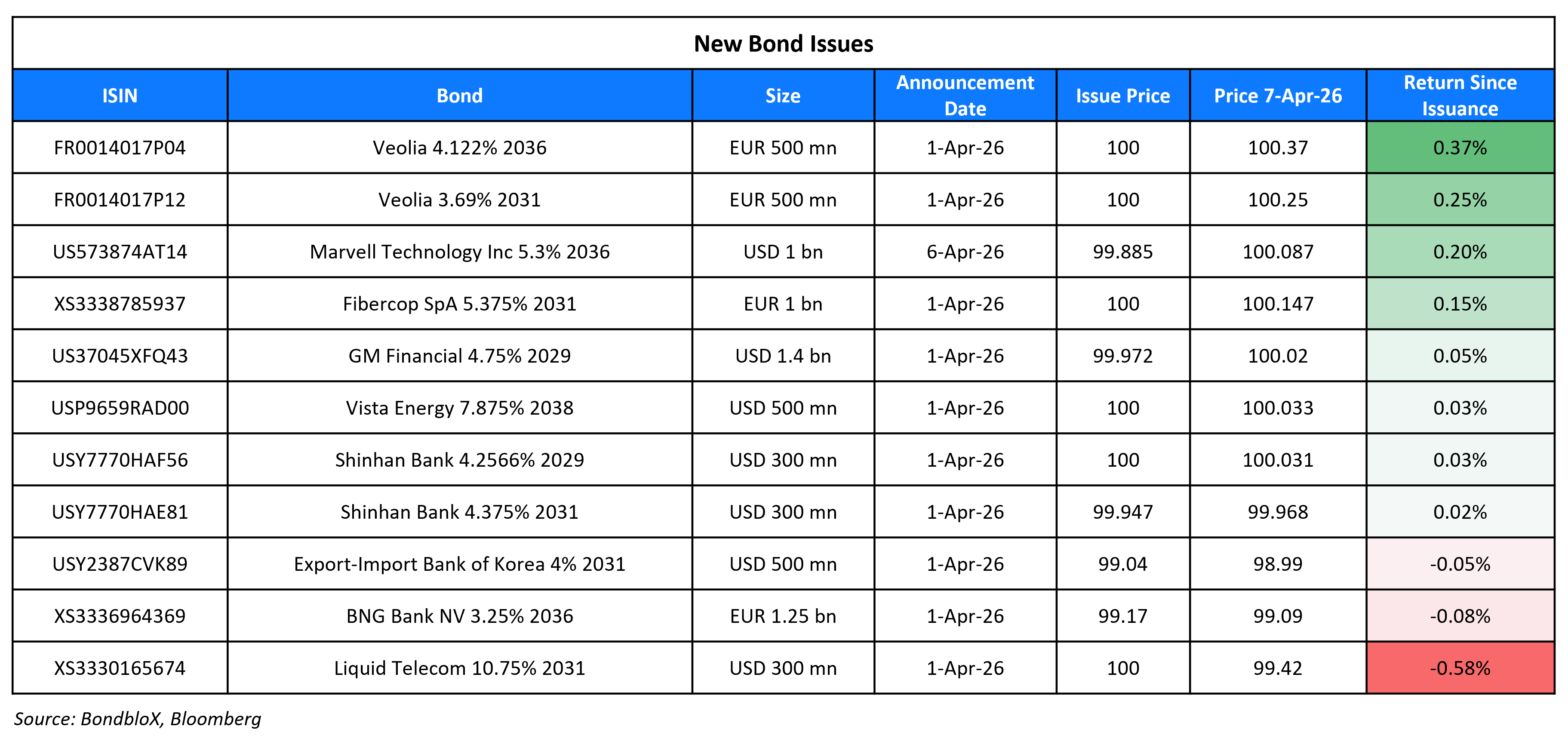

New Bond Issues

Marvell Technology raised $1bn via a 10Y bond at a yield of 5.315%, 28bp inside initial guidance of T+125bp area. The senior unsecured note is rated Baa2/BBB/BBB+. Proceeds will be used for general corporate purposes, including working capital funding, dividend payments, capex, share buybacks, debt repayment and acquisitions. The company may temporarily invest funds that are not immediately needed for these purposes in short-term investments.

New Bonds Pipeline

- Sasol $ 7NC3 bond

Rating Changes

- Moody’s Ratings upgrades Crocs CFR to Ba2

- Fitch Downgrades JetBlue to ‘CCC+’ from ‘B-‘; Affirms and Downgrades Certain EETC Ratings

- Fitch Places Qatari Banks on Rating Watch Negative

- Moody’s Ratings affirms Campbell’s Baa2, P-2 ratings, outlook changed to negative

Term of the Day: Sukuk

Talking Heads

On warning that Iran war may drive inflation and rates higher – Jamie Dimon, JPMorgan CEO

“Now, because of the war in Iran, we additionally face the potential for significant ongoing oil and commodity price shocks, along with the reshaping of global supply chains, which may lead to stickier inflation and ultimately higher interest rates than markets currently expect”

On Middle East war leading to higher prices, slower growth – Kristalina Georgieva, IMF MD

“Instead, all roads now lead to higher prices and slower growth…We are in a world of elevated uncertainty… All of this means that after we recover from this shock, we need to keep our eyes open for the next one… Even if the war is to stop today, there would be a lingering negative impact to the rest of the world.”

On Chatter About Fed’s Balance Sheet Ahead of Reality – CIBC

“Having a reserve scarcity will not create material benefits from building an active market… Given that two triggers are needed to cause a dramatic rate spike (scarce reserves and a supply/demand mismatch), it is almost impossible for the Fed to know precisely when it is crossing from ample reserves to scarce reserves.”

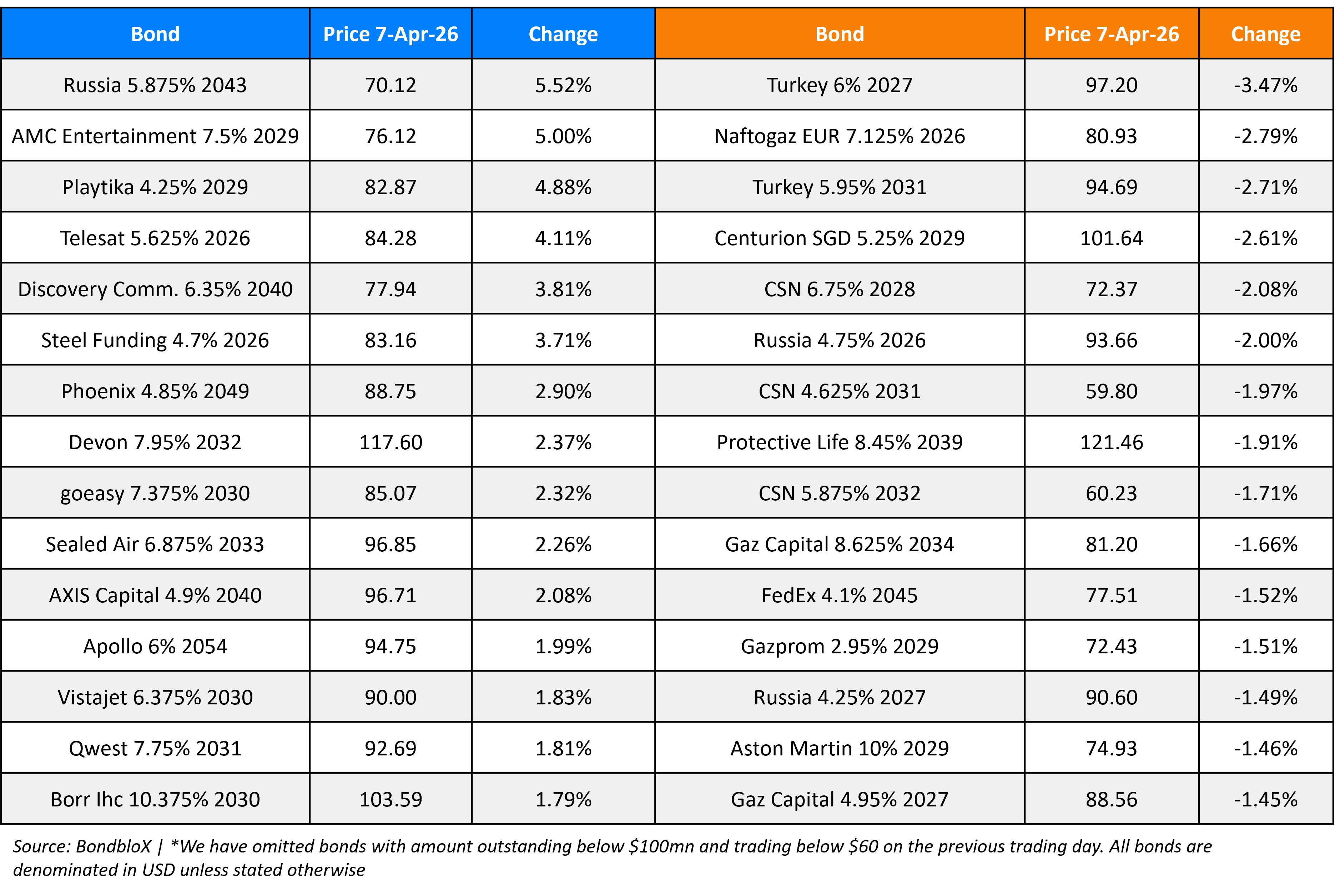

Top Gainers and Losers- 07-Apr-26*

Go back to Latest bond Market News

Related Posts:

Our Awards

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.