This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

Fed Keeps Rates Unchanged; Treasury Yields Jump Higher

March 19, 2026

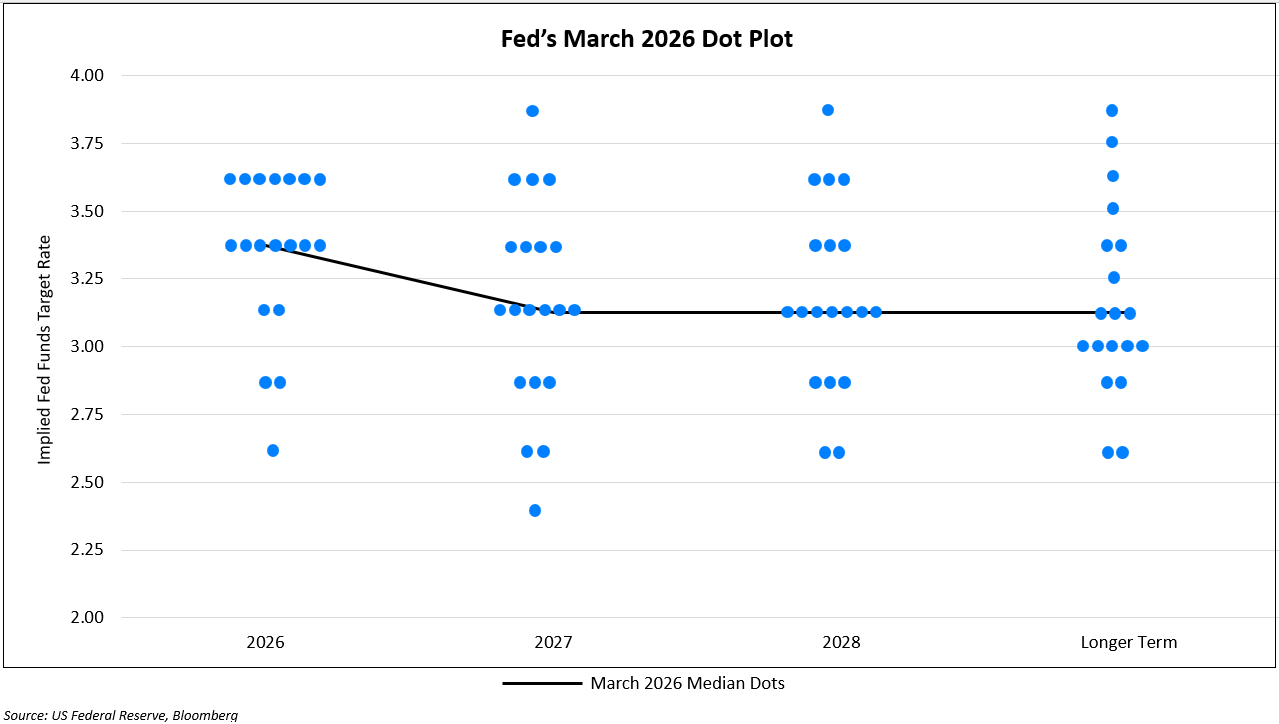

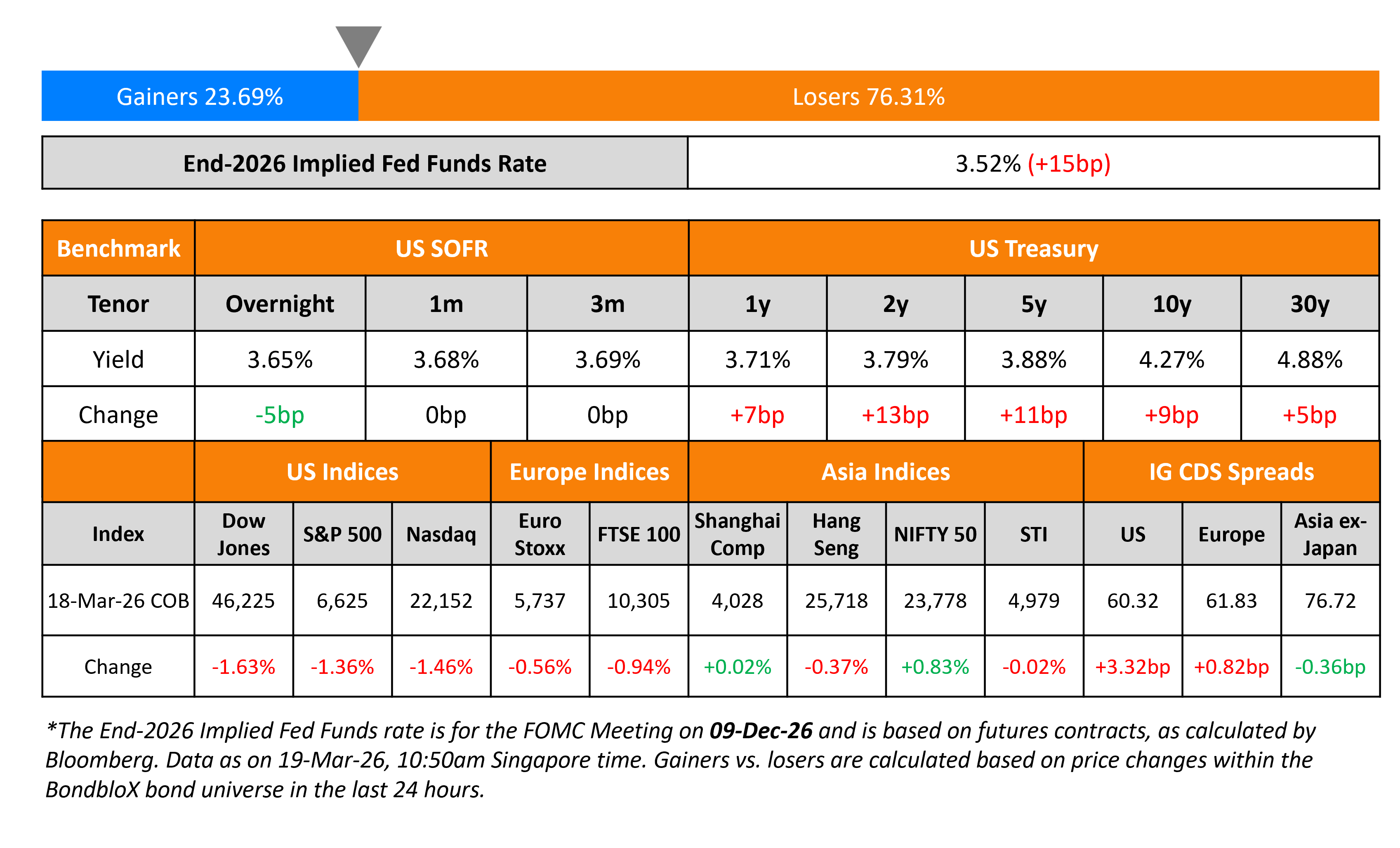

US Treasury yields shot higher with the 2Y yield up by 13bp and the 10Y up 9bp, on the back of the FOMC and the escalation in geopolitical tensions. The FOMC meeting saw a 11-1 vote in favor of no change to the Fed Funds Rate, with Stephen Miran being the only dissenter voting for a rate cut. The Fed’s Dot Plot (image below) indicated that the median Fed Funds Rate for 2026 was unchanged from the December meeting, with one rate cut being expected this year. However, the distribution saw “a meaningful amount of movement — toward fewer cuts by people”, as noted by Chairman Jerome Powell. The dot plot also showed that the Fed expects another 25bp rate cut in 2027 post which it does not see any major change to its median policy rate.

The Summary of Economic Projections showed that the Fed’s forecast for the change in real GDP rose to 2.4% from 2.3% in December, with the unemployment rate expected to hold steady at 4.4%. The Core PCE projection climbed to 2.7% for 2026, up from 2.5% in December. Besides, Powell hinted that tariffs were keeping inflation elevated along with the recent geopolitical tensions in the Middle East.

On the geopolitical front, Iran launched missile and drone strikes on Qatar’s Ras Laffan Industrial City, with extensive damage being reported. The Ras Laffan plant is the world’s largest LNG production plant that produces one-fifth of global LNG supply. Saudi Arabia also reported that two of their refineries were attacked. Iran said that its strikes were driven in retaliation after its South Pars gas field was hit by US-Israel. Brent crude shot up to over $110/bbl. Markets are now pricing-in only 12bp in Fed rate cuts for 2026 vs. a 25bp cut a few days earlier.

Looking at US equity markets, the S&P and Nasdaq ended lower by 1.4% and 1.5% respectively. US IG CDS spreads widened by 3.3bp and HY CDS spreads were 16.8bp wider. European equity indices ended lower too. The iTraxx Main CDS spreads were 0.8bp wider and the Crossover CDS spreads were 4.2bp wider. Asian equity markets have opened in the red this morning. Asia ex-Japan CDS spreads tightened by 0.4bp.

New Bond Issues

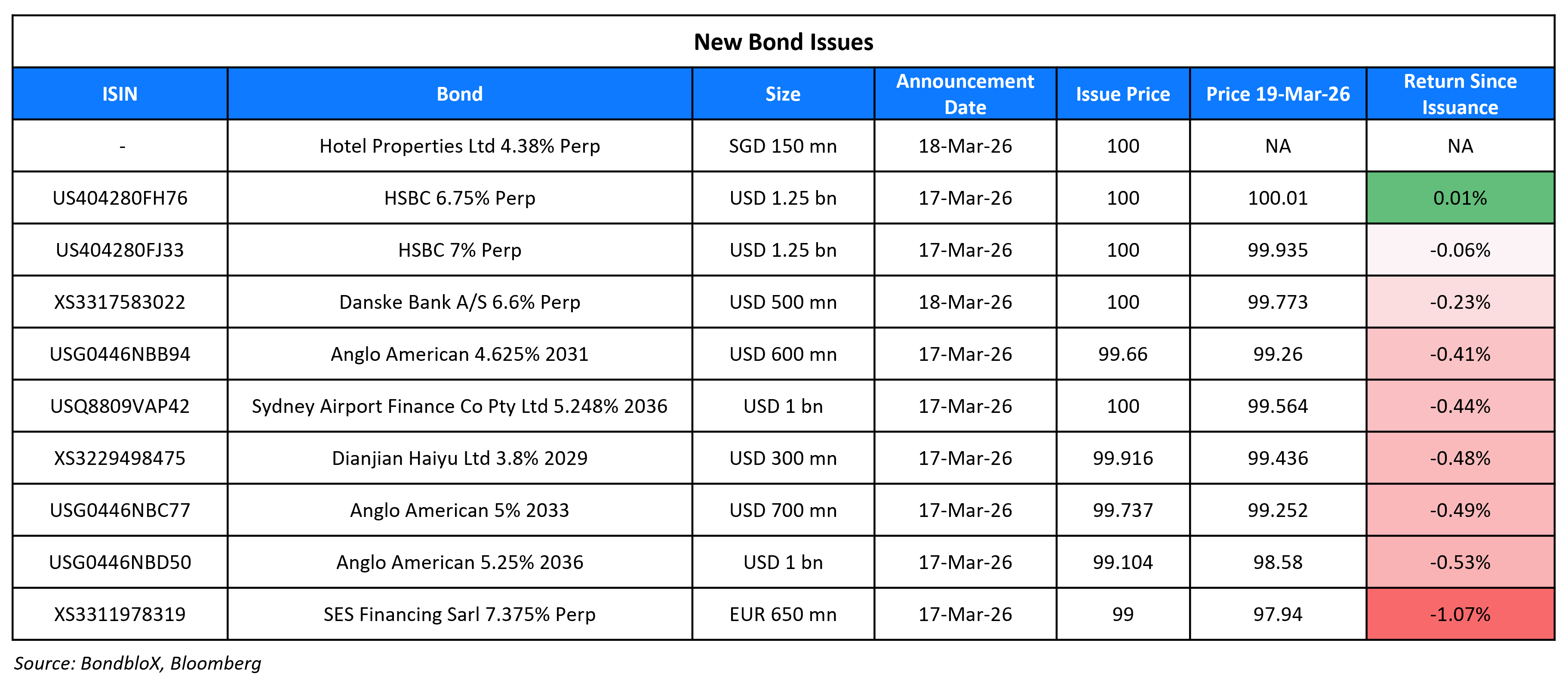

Hotel Properties raised S$150mn via a PerpNC5 bond at a yield of 4.38%, 22bp inside initial guidance of 4.60% area. The subordinated note is unrated. If not called by 25 March 2031, the coupon will reset to the 5Y SORA-OIS plus 259.7bp. There is also a coupon step-up of 100bp if not called. If there is a change of control event and the bond is not called, the coupon will step-up by an additional 300bp. The notes have a dividend stopper. Proceeds will be used to refinance existing borrowings and finance working capital requirements.

Danske Bank raised $500mn via a PerpNC7 AT1 bond at a yield of 6.6%, ~58.75bp inside initial guidance of 7.125-7.25% area. The junior subordinated note is unrated. If not called by 25 September 2033, the coupon will reset to the US 5Y Treasury yield plus 255.1bp. A trigger event will occur if the CET1 Ratio of the issuer and/or the group, at any time, falls below 7%.

New Bonds Pipeline

- Kexim $ 3Y/5Y bond

- Korea National Oil Corp $ bond

Rating Changes

- Moody’s Ratings upgrades Bolivia’s ratings to Caa3 and changes outlook to positive

- Fitch Upgrades Tenet’s IDR to ‘BB’; Outlook Stable; Resolves UCO

- Companhia Siderurgica Nacional Downgraded To ‘B’ Amid Persistently High Leverage; Outlook Negative

- Moody’s Ratings Downgrades Raizen to Ca; stable outlook

- Italy-Based Mediobanca Downgraded To ‘BBB’ On Higher Risks; Outlook Positive

- Deutsche Pfandbriefbank AG ‘BBB-/A-3’ Ratings Affirmed; Some Hybrids Downgraded; Outlook Remains Negative

- Fitch Places Omniyat on Rating Watch Negative

Term of the Day: Collateralized Loan Obligations (CLO)

Collateralized Loan Obligations (CLO) are securities backed by a pool of underlying loans. The loans are packaged together by a process of securitization. The loans are bundled together in tranches in an order of risk – for example, the AAA rated tranche comes with the lowest default risk while a BB tranche has a higher default risk. Investors can choose the tranche they prefer based on risk appetite. Given that the underlying loans are floating rate loans, they are also considered a hedge against inflation.

Talking Heads

On Oil-Driven Inflation Fears Reshaping Asian Bond Yield Curves

Goldman Sachs strategists

“We think Asian rates curves are more likely to bull-steepen or pivotally steepen from here”

Wee Khoon Chong, BNY

“The curve flattening has probably run its course as we do not see rate hikes as an effective strategy to address supply-shock-triggered high inflation… policy focus will soon shift to supporting growth than fighting inflation”

On Fed Signal Is ‘Don’t Worry About It’ – Bob Michele, JPMorgan

“They’re telling us don’t worry about it. There is a real impact to inflation and ultimately the labor market… Personally, I think he will stay on past the midterms… him staying on, I think, creates stability.”

On Bond Traders Scaling Back 2026 Fed Rate Cut Bets on Oil, PPI

Elias Haddad, Brown Brothers Harriman

“The sticky US inflation backdrop leaves the Fed with little room to look through the oil shock, tilting the balance toward less easing”

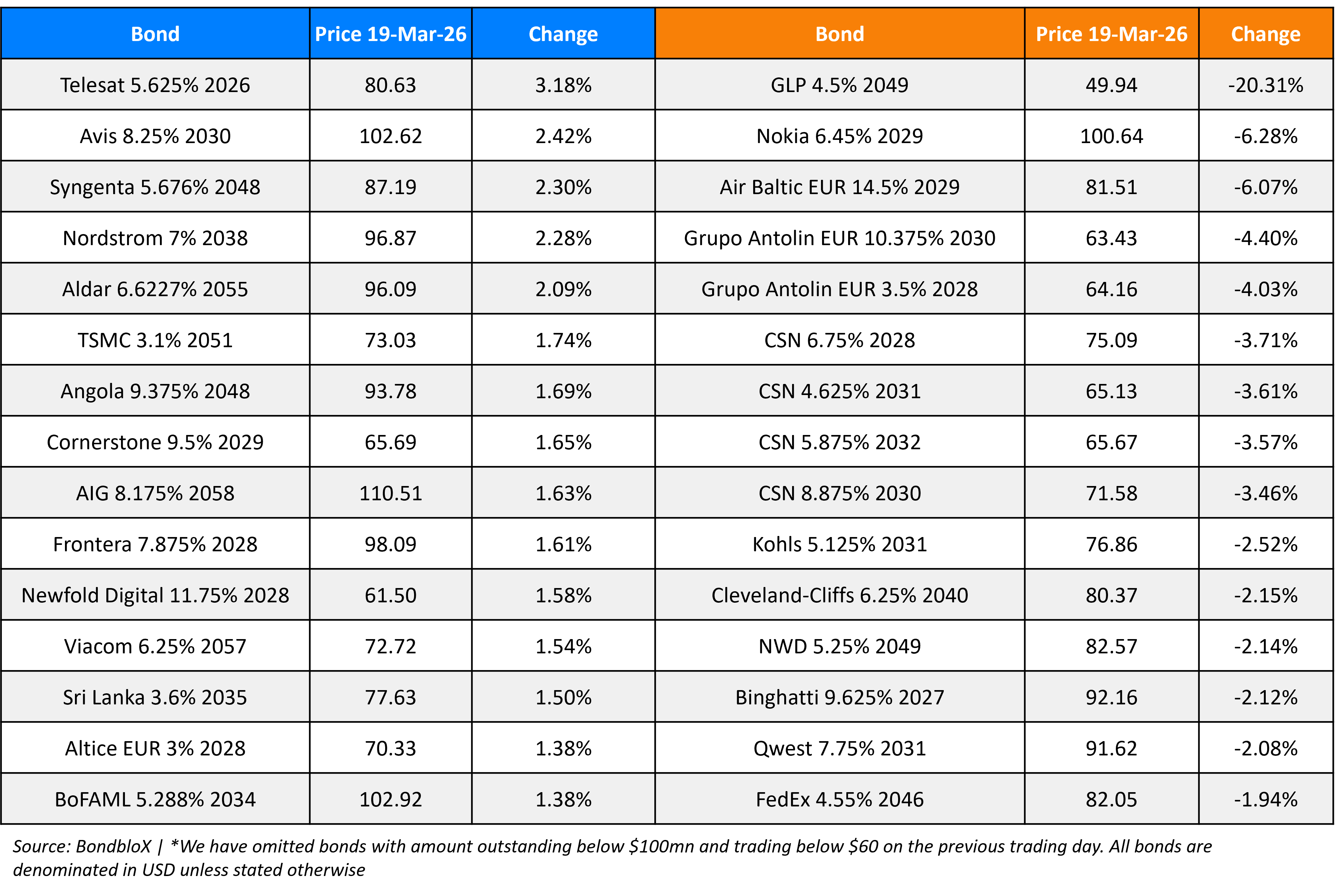

Top Gainers and Losers- 19-Mar-26*

Go back to Latest bond Market News

Related Posts:

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.