This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

Bond Market News

February 2026: 90% of Dollar Bonds Rally in February as Treasury Yields Shift Sharply Lower

March 2, 2026

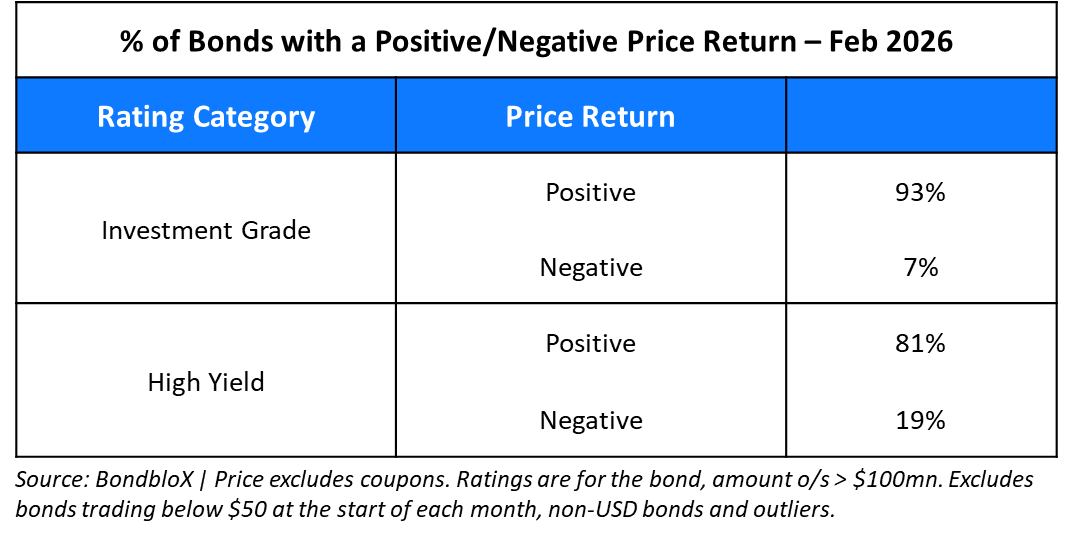

February 2026 was a solid month for bond investors, with 90% of dollar bonds ending higher (price returns ex-coupons). 93% of Investment Grade (IG) bonds ended in the green, outperforming High Yield (HY) bonds where 81% ended in the green. This came on the back of weakening geopolitical sentiment and equity market volatility. Markets are currently pricing-in nearly 60bp in Fed rate cuts by the end of the year.

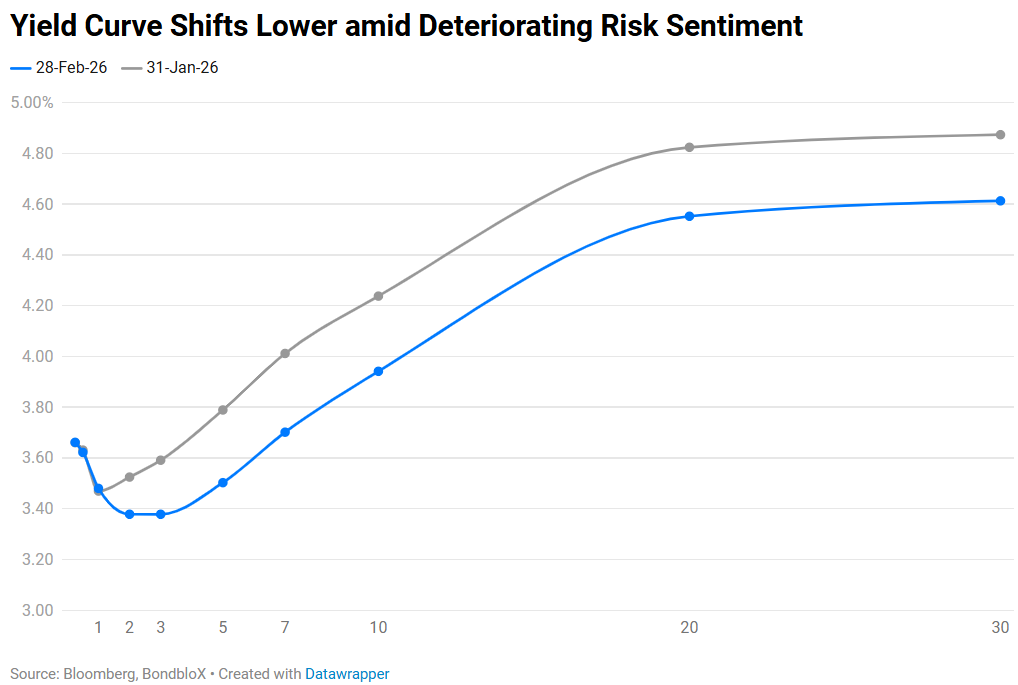

The month of February saw the Treasury yield curve shift lower sharply. This was led by the 5Y and 10Y yields dropping by nearly 30bp. On the inflation front, US CPI in January rose by 2.4% YoY vs. expectations of 2.5% and the prior month’s 2.7% print. The Core CPI rose by 2.5% YoY, inline with expectations, but lower than the prior month’s 2.6% print. This was the core inflation’s lowest reading since March 2021. However, on the geopoltical front, the US imposed global tariffs of 15%, post which US-Iran uncertainty weighed on the markets. Besides, concerns about AI impacting tech and other industres pulled equity markets down.

However, most of the other macroeconomic data from the US provided a solid economic backdrop. NFP for January showed a sharp jump, coming in at 130k, beating expectations of 65k and the prior month’s 48k print. The Unemployment Rate fell to 4.3% vs. expectations of 4.4%. Average Hourly Earnings (AHE) YoY rose by 3.7%, in-line with expectations. The ISM Manufacturing Index surged to 52.6 in January, jumping from 47.9, hitting a 40-month high. This was also its first reading in expansionary territory since February 2025.

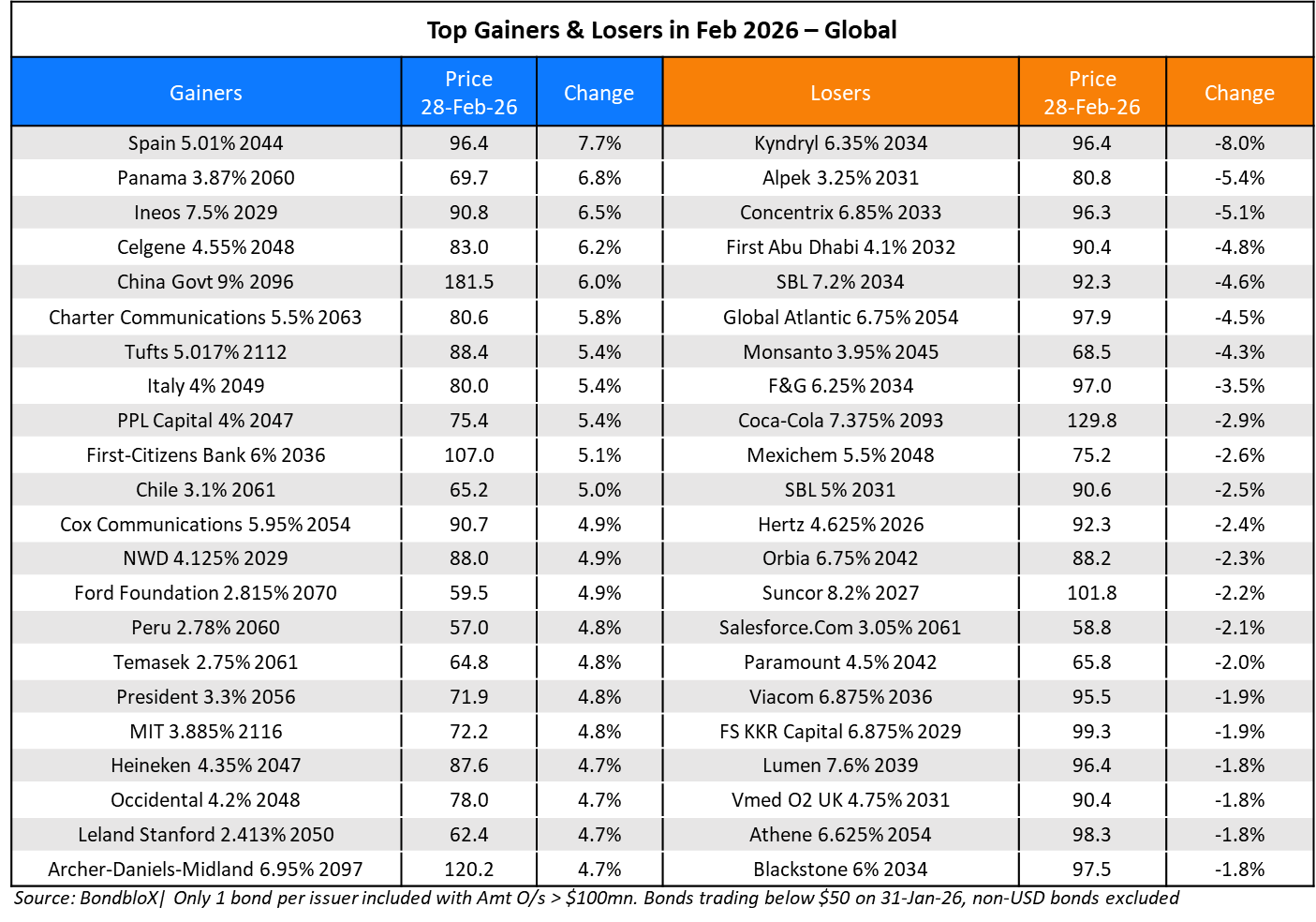

In the AAA to A- rated IG space, ultra long-dated bonds (maturing beyond 2050) of sovereigns like Panama, Peru, Chile, Spain, China etc. and companies like Charter Communications, Occidental and others ticked higher by over 5%. However, among the losers, Kyndryl’s notes fell by over 5% during the month, followed by Alpek, Concentrix and F&G.

Frontera Energy’s dollar bond was the top gainer in the high-yield (HY) category, rising 31% over the last month. The move came after GeoPark signed a deal to buy Frontera’s oil and gas assets in Colombia for up to $400mn plus assumed debt. Tullow Oil’s bond was the second best performer, gaining 15% after the company reached a refinancing agreement supported by about two-thirds of its bondholders and lender Glencore Energy UK Ltd. to delay the principal repayment on the bond. NWD’s Perps were also among the top gainers, surging 8–14% after the developer announced the launch of three new residential projects in 1H2026. Bonds of other Hong Kong-based developers, like Lai Sun and Far East also rallied by 10% during the month. Ineos bonds gained 5–11% last month after the EU crack down on cheap imports by foreign companies. Senegal’s dollar bonds also rallied by 6-8% after the country secured funding to meet eurobond payments due in March. MetInvest’s dollar bonds gined by 7-13% after it launched Investor roadshows to gauge appetite for a new bond issuance.

Raizen’s dollar bonds were the top loser in the category, dropping 40-43% during the month. The move came after all three rating agencies downgraded its credit ratings by multiple notches. Vista Land’s dollar bonds also lost 23-30% of their value last month after the Philippine SEC filed a criminal complaint against the promoter and the company’s directors for alleged market manipulation and insider trading. Xerox’s dollar bonds continued to trend lower, dropping 13-35%, after the company launched a major balance-sheet restructuring aimed at cutting debt and restoring financial stability. CSN bonds also dropped by 10-15%, as Brazil’s corporate debt market was shaken by a sharp sell-off following Raizen’s dramatic credit downgrades. CSN was also downgraded to B2 by Moody’s two weeks back.

Issuance Volumes

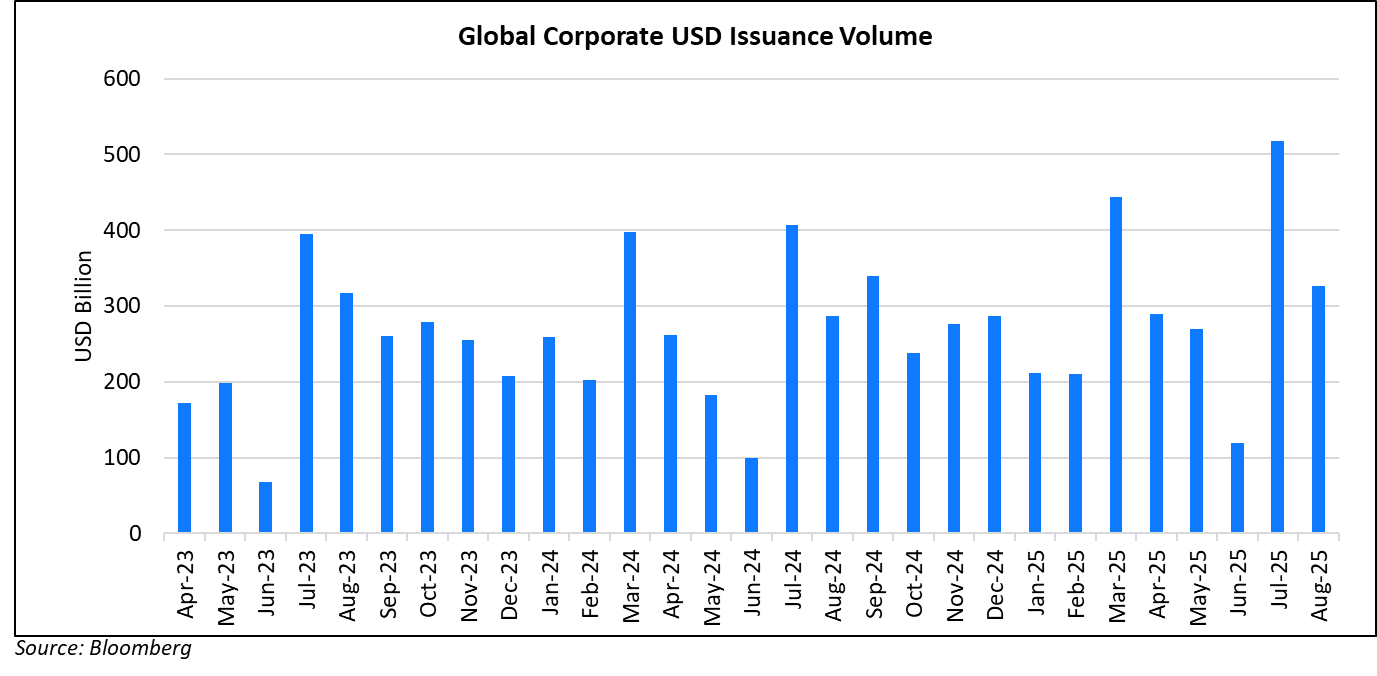

Global corporate dollar bond issuances stood at $326.2bn in February, 37% lower MoM. As compared to February 2025, issuance volumes were up 14%. 82% of the issuance volumes came from IG issuers with HY comprising 15% and unrated issuers taking the remaining 3%.

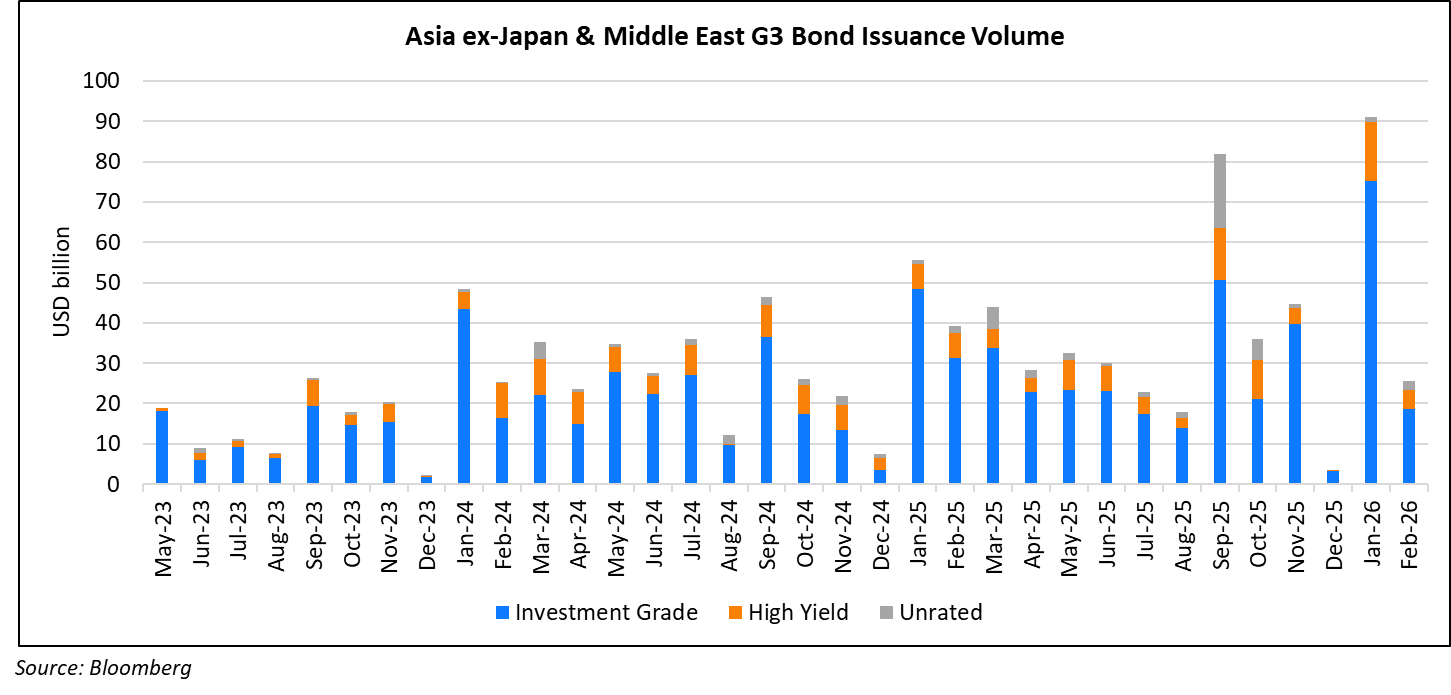

Asia ex-Japan & Middle East G3 issuance stood at $25.5bn, down 72% MoM and 35% YoY. 73% of the volumes came from IG issuers with HY issuing 19% and unrated issuers taking the rest.

Largest Deals

The largest deals globally were dominated by large American companies. Oracle’s $25bn eight-part deal led the tables, followed by Alphabet’s $20bn seven-part deal and Abbott Labs’ $20bn eight-part deal. Big banks also contributed to a significant chunk of the volumes — this included BofA’s $7bn three-trancher, UBS’ $5.25bn four-trancher, Barclays and Lloyds’ $4bn multi-tranche deals among others. Other large deals included Brazil’s $4.5bn two-part issuance, AbbVie’s $8bn seven-trancher, SV RNO’s $7.6bn deal, Walt Disney and Amgen’s $4bn issuances each among others.

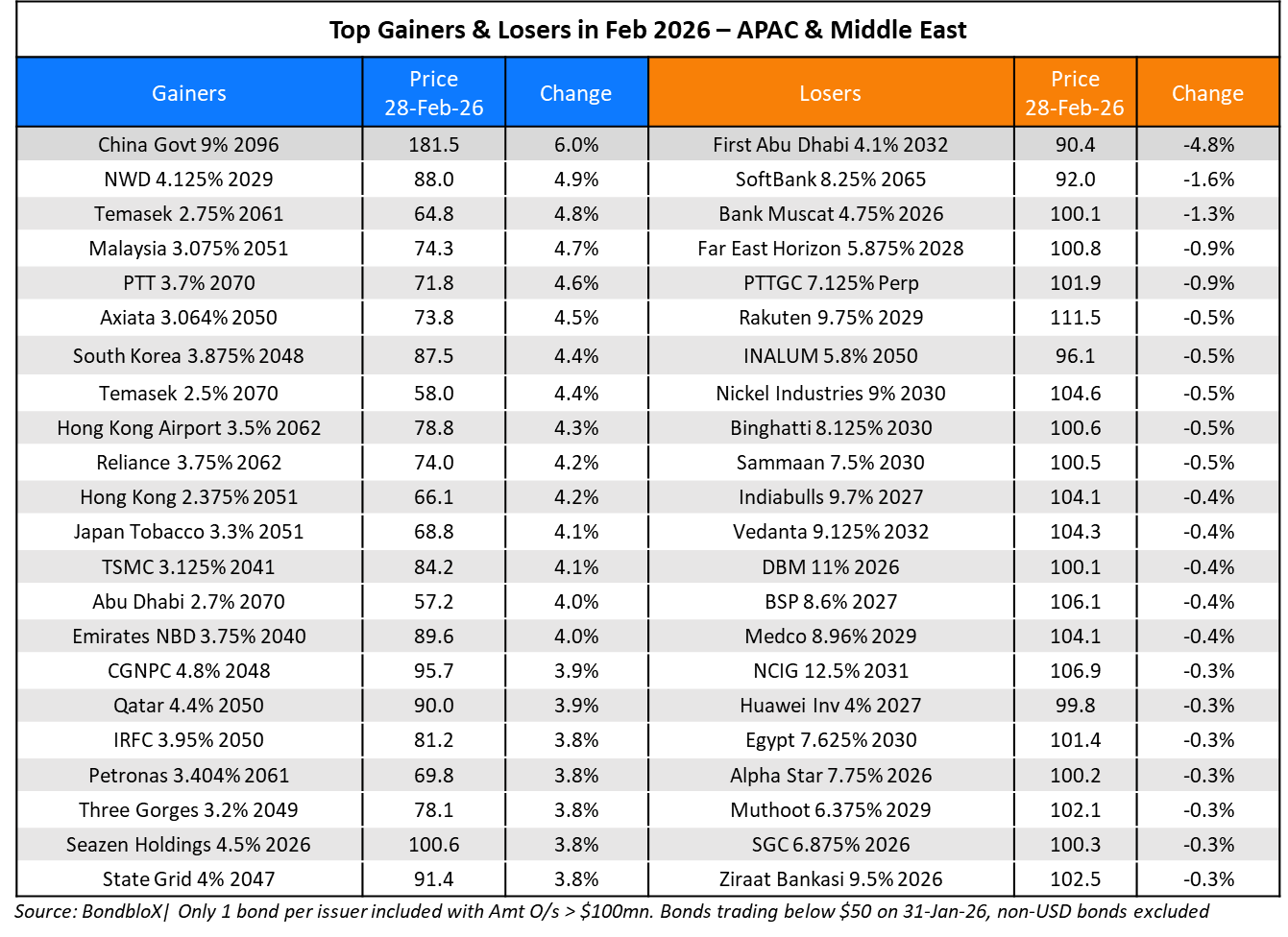

In the APAC and Middle East region, deal volumes were led by Abu Dhabi’s $3bn two-trancher, followed by Korea’s $3bn two-part issuance, Indonesia’s €2.7bn three-part issuance, CICC’s $1.4bn two-part deal, NAB’s $1.43bn multi-currency issuance and Advanced Info Services’ $1bn two-trancher.

Top Gainers & Losers

Go back to Latest bond Market News

Related Posts:

High-Yield Bonds Lead The July Recovery

August 6, 2018

Bond Yields – Explained

December 26, 2024

What to Look for When Buying Bonds

December 4, 2024

BondbloX Pte. Ltd. is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.